Priority Centered Management

Moving from a historical allocation model to a Priority Centered Management (PCM) model will allow the university to ensure sufficient reserves, invest in priorities, and better support decentralized program innovation geared toward advances in strategic priorities for the university.

The model also uses different mechanisms to determine allocations, one for academic units and one for the support units. Academic units are most directly affected by the different formulas as a portion of their formula is tied to Student Credit Hours (SCH). Increases or decreases in course enrollment and majors will affect the revenue of academic units at the College and School level. These units will also receive a portion of their revenue based on performance related to institutional strategic priorities.

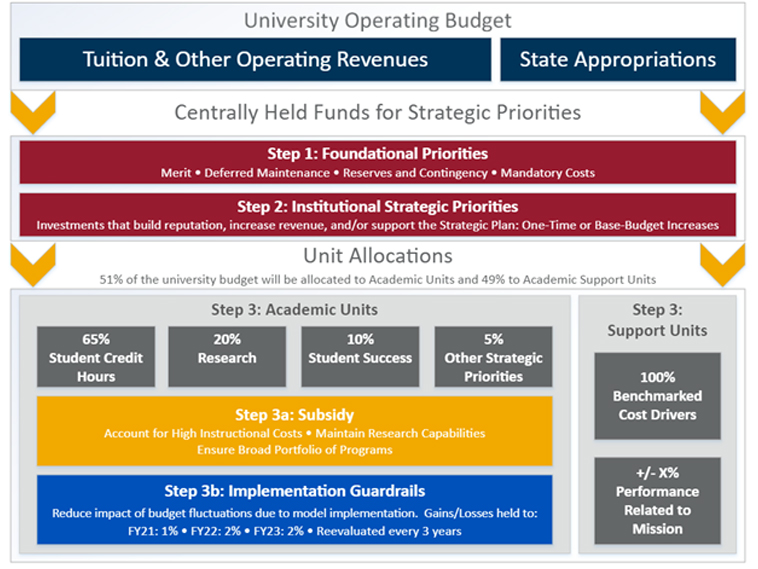

Institutional Overview: The 1-2-3 of the new priority centered management budget allocation model

The first structural feature of the model is the creation of three broad categories in which budgetary resources can be allocated. The source of these funds includes state appropriations, tuition revenue, and certain other operating revenues.

Funding streams — such as course fees and differential tuition, fees charges for services — will be allocated directly to the applicable unit and are not part of this budget allocation model or the pool of funds being distributed. KU Endowment Funds available to various campus offices are separate from the budget model and do not figure into the unit revenue allocation process.

Step 1: Budget allocated to foundational priorities

Step 2: Budget allocated to institutional strategic priorities

Step 3: Budget allocated to academic units and support units. This step includes funds set aside to subsidize units and uses separate formulas for academic units and support units.

![[enlarge image]](https://provost.cms-dev.ku.edu/sites/provost/files/images/PCM%20Budget%20Model/Budget_Model_123_20191205.jpg){kind=link}

Step 1: Set aside revenue for Foundational Priorities

The Chancellor and Provost will set aside a portion of funds from state appropriations and tuition revenue. Funds will be used to support central foundational priorities, such as:

- Restoration of savings/reserves and contingency funds

- Regular merit raises that flow through to unit budgets

- Deferred maintenance needs

- Increased year-to-year mandatory costs (fringe benefit costs, utilities, external licensing, subscriptions, etc.)

Step 2: Set aside revenue for Strategic Priorities

Strategic priorities are areas that are part of KU’s vision, future goals and growth. The funds are held by the Chancellor and the Provost and are expected to be used for one- time or limited-term investments that can build reputation or revenue opportunities. These may also be used to support initiatives determined through the strategic planning process.

Step 3: Allocation of revenue to campus units

This distribution will provide resources needed by each academic unit (the schools and the College) and support units that provide crucial services to students, faculty, and staff. Based on the expected allocation for Stepps 1 and 2 for the upcoming fiscal year, the pool for allocation is approximately $405 million. Initially, roughly 51% of remaining funds will be allocated to academic units and 49% will be allocated to support units.

There will be two distribution methods:

1) Equation-based allocation to the Schools/College

- The process uses subsidy to support units that have high instructional costs, that need to maintain research capabilities, and/or that may be unable to grow through traditional or nontraditional enrollment efforts.

- Initially, the model will set aside $20 million for purposes of subsidy

- In initial years of budget model implementation, guardrails will be used to ensure gains and losses for each unit are minimized/stabilized.

2) Benchmarked and performance-based allocation to support units

- Initially the support units will be assigned to receive 100 percent of their previous year’s budget, which will remain in effect until reliable benchmarked estimates are able to be calculated for each unit, at which point the allocations may shift based on benchmarking data.

- Units will be eligible to receive more or less depending on each unit’s performance related to its mission.

- Implementation of the new priority centered budget model for support units will be conducted separately from that of the academic units so the university can conduct benchmarking of service unit activities in comparison with peer and aspirational institutions.